Health insurance in the United States often feels like a luxury instead of a basic need. Prices keep rising, plans get more confusing, and many people feel stuck paying high monthly premiums without even using their coverage. That frustration pushed me to do something different. I wanted to see if it was actually possible to find cheap health insurance in USA without sacrificing essential coverage.

What I discovered surprised me. The price gap between plans is massive, and with the right strategy, you can save hundreds of dollars every month. Most people overpay simply because they don’t know where to look or how to compare plans properly. That’s exactly what I set out to fix.

In this article, I will walk you through everything I learned during my search. You’ll see the lowest health insurance cost USA options available right now, how I found them, and what you should watch out for before choosing a plan. I will also break down real numbers, including premiums, deductibles, and out-of-pocket costs, so you can understand the full picture.

If you’re tired of overpaying and want affordable health plans USA that actually make sense, you’re in the right place. Let’s get into it.

What is Health Insurance in the USA

Health insurance in the United States is a system that helps you pay for medical expenses. Instead of covering the full cost of doctor visits, hospital stays, or prescriptions, you pay a monthly fee called a premium, and the insurance company shares the cost when you need care.

At first glance, it sounds simple. But once you dive deeper, it becomes clear that the system has layers of complexity. Different plans offer different levels of coverage, and the cheapest option is not always the best one for your situation.

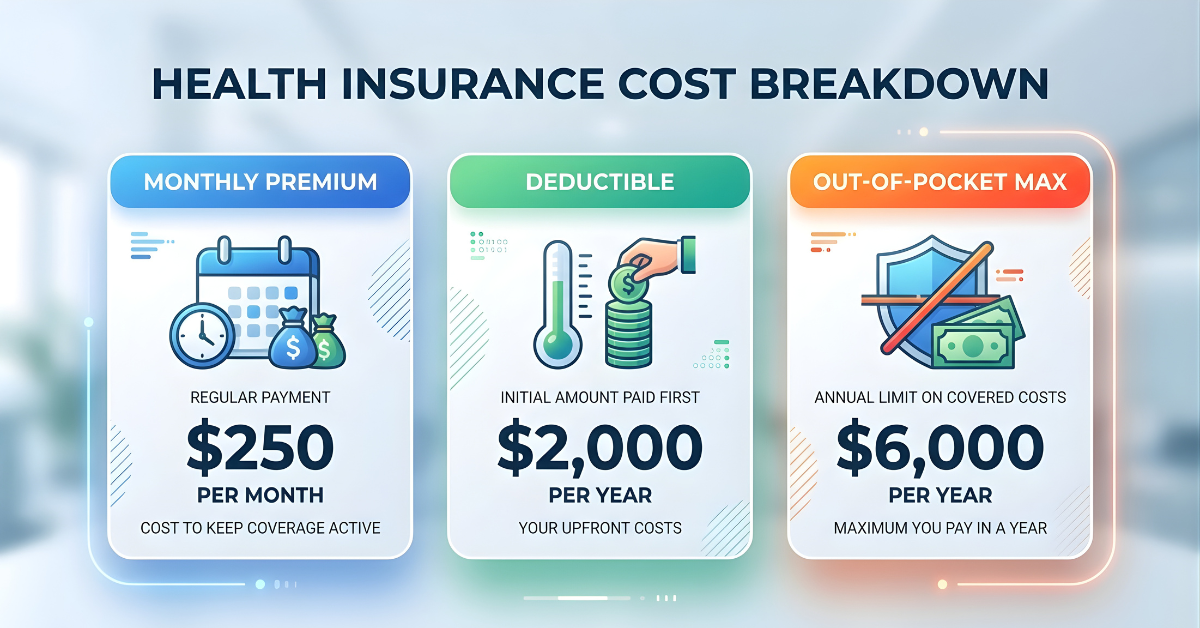

Most plans in the US include several key cost components:

- Monthly premium

- Deductible

- Copayments

- Coinsurance

- Out-of-pocket maximum

Understanding these elements is crucial if you want to find the best budget health insurance USA. Many people only focus on the monthly premium, but that can be misleading. A plan with a low premium might have a very high deductible, which means you pay more when you actually need care.

Health insurance is also tied closely to employment in the US. Some people get coverage through their employer, while others buy plans through the Health Insurance Marketplace or private providers. Government programs like Medicaid and Medicare also provide coverage for eligible individuals.

Knowing how the system works is the first step toward finding a cheaper plan that still protects you financially.

How It Works

Health insurance works like a cost-sharing agreement between you and the insurer. You pay a fixed amount every month, and in return, the insurance company helps cover your medical expenses. But the way costs are split can vary a lot depending on your plan.

For example, before your insurance starts paying, you often need to meet your deductible. This means you cover medical expenses out of your own pocket up to a certain amount. After that, the insurance company begins to share the costs through coinsurance or copays.

Let’s say your deductible is $2,000. If you have a medical bill for $1,500, you pay the full amount. If your bill is $3,000, you pay the first $2,000, and then your insurance starts covering a portion of the remaining $1,000.

Another important part is the out-of-pocket maximum. This is the most you will pay in a year for covered services. Once you reach this limit, your insurance covers 100% of eligible expenses.

Understanding these mechanics helped me compare affordable health plans USA more effectively. I realized that the cheapest plan upfront might not be the cheapest overall, especially if it comes with high hidden costs.

Types of Health Insurance Plans

There are several types of health insurance plans in the US, and each one has its own structure and pricing. Choosing the right type can make a big difference in how much you pay.

The most common plan types include:

- HMO (Health Maintenance Organization)

These plans usually have lower premiums but require you to use a network of doctors and get referrals for specialists. - PPO (Preferred Provider Organization)

These plans offer more flexibility in choosing doctors but come with higher premiums. - EPO (Exclusive Provider Organization)

A mix between HMO and PPO, with moderate costs and limited network flexibility. - HDHP (High Deductible Health Plan)

These plans have low monthly premiums but high deductibles. They are often paired with Health Savings Accounts (HSAs).

During my search for the lowest health insurance cost USA, I found that HDHP plans were often the cheapest in terms of monthly premiums. However, they also carried higher risks if unexpected medical expenses came up.

Choosing the right type depends on your health needs, budget, and risk tolerance. A healthy individual might benefit from a low-cost plan, while someone with ongoing medical needs might need more comprehensive coverage.

Why Health Insurance is Expensive in 2026

Health insurance costs in the US continue to rise, and 2026 is no exception. Many people wonder why prices keep increasing even when they rarely use their insurance. The answer lies in several key factors that drive costs upward.

One of the biggest reasons is the rising cost of medical care. Hospital stays, surgeries, and prescription drugs are more expensive than ever. Insurance companies adjust their prices to cover these growing expenses, which leads to higher premiums for consumers.

Another factor is administrative complexity. The US healthcare system involves multiple players, including providers, insurers, and government agencies. Managing all these interactions adds overhead costs that ultimately get passed on to policyholders.

There is also the issue of risk pooling. Insurance works by spreading risk across many people. When more individuals require expensive treatments, insurers raise premiums to balance the risk.

Understanding these factors helped me see why finding cheap health insurance USA requires more than just picking the lowest price. You need to look at the full structure of the plan and how it aligns with your needs.

Rising Medical Costs

Medical costs in the US have been climbing steadily for years, and 2026 continues this trend. According to recent data, healthcare spending in the US exceeds $4 trillion annually, making it one of the most expensive systems in the world.

Hospitals charge high fees for services, and prescription drug prices are significantly higher compared to other countries. These costs directly impact insurance premiums.

For example, a simple emergency room visit can cost over $1,500 without insurance. With insurance, you might still pay hundreds depending on your plan. These high baseline costs force insurers to increase premiums to stay profitable.

This reality makes it even more important to find affordable health plans USA that balance cost and coverage effectively.

Inflation and Policy Changes

Inflation also plays a major role in rising health insurance costs. As the overall cost of living increases, so do medical expenses, wages for healthcare workers, and operational costs for providers.

Policy changes can also affect pricing. Government regulations, subsidies, and tax policies influence how insurance companies set their rates. For example, changes in subsidy eligibility can impact how much individuals pay for marketplace plans.

During my search, I noticed that subsidies made a huge difference in finding the best budget health insurance USA. Some plans that seemed expensive at first became very affordable after applying available credits.

How I Found the Cheapest Plan

Finding the cheap health insurance USA option that actually works is not about luck. It is about knowing where to look, what to compare, and how to avoid traps that make a plan look cheaper than it really is. I did not just pick the lowest monthly premium and call it a day. I went deeper, compared multiple factors, and tested different scenarios to see what I would actually pay in real life.

I started with a simple question: what is the lowest health insurance cost USA that still offers basic protection? That question guided my entire process. I focused on plans that covered essential benefits but did not include unnecessary extras that increase premiums.

One thing became clear quickly. Many people overpay because they stay with the same provider year after year. Insurance companies often raise prices quietly, and unless you actively compare plans, you might not notice how much you are losing. I treated this like shopping for a flight ticket. I checked multiple sources, compared features, and stayed flexible with my choices.

I also looked at my own health habits. I rarely visit doctors, and I do not take regular medication. That allowed me to consider high-deductible plans that offer lower monthly costs. If your situation is different, your “cheapest” plan might look very different from mine.

By the end of my search, I realized that the cheapest plan is not a fixed answer. It depends on your income, health, and eligibility for subsidies. Still, there are clear strategies that can help almost anyone reduce their costs significantly.

Research Strategy

My research strategy was simple but effective. I broke the process into steps and followed them carefully instead of rushing into a decision. First, I used the official Health Insurance Marketplace to check available plans in my area. This is where many people qualify for subsidies, which can drastically reduce premiums.

Next, I compared at least five plans side by side. I did not just look at the monthly premium. I checked:

- Deductibles

- Out-of-pocket maximums

- Network coverage

- Prescription benefits

Then, I calculated the “worst-case scenario” cost for each plan. This means adding the annual premium plus the maximum out-of-pocket cost. This step changed everything. Some plans that looked cheap upfront turned out to be expensive in real situations.

I also paid attention to provider networks. A cheap plan is useless if your nearest hospital is not covered. I made sure the plans included basic access to local healthcare providers.

This approach helped me filter out misleading options and focus on truly affordable health plans USA that balance cost and usability.

Tools and Platforms Used

To find the best budget health insurance USA, I used a mix of official and private tools. Each platform gave me different insights, and combining them helped me make a better decision.

The main platforms I used included:

- Healthcare.gov (for marketplace plans and subsidies)

- Private insurer websites (for direct plan comparisons)

- Comparison tools like Policygenius and eHealth

Healthcare.gov was the most important tool. It showed me real prices after subsidies, which made a huge difference. Some plans dropped by over 50% after applying tax credits.

Private comparison tools helped me understand plan features more clearly. They often present data in a more user-friendly way, which made it easier to compare options quickly.

I also checked reviews and user experiences. While reviews are not always perfect, they gave me a sense of how reliable each provider is.

Using multiple tools ensured that I did not miss hidden opportunities. It also helped me confirm that I was truly getting the lowest health insurance cost USA available for my situation.

Exact Cost Breakdown

After hours of research and comparisons, I finally found a plan that stood out as the cheapest realistic option. But instead of just sharing the monthly premium, I want to break down every cost involved. This is where most people make mistakes.

The total cost of health insurance is not just what you pay each month. It includes several layers that only become visible when you actually use the plan. Understanding these layers helped me avoid surprises and choose a plan that fits my budget.

The plan I selected is a high-deductible marketplace plan with subsidy support. It is not the most comprehensive plan, but it offers essential coverage at a very low cost. For someone with minimal healthcare needs, it makes financial sense.

Let’s break down the numbers clearly so you can see what I actually pay and what I might pay in the worst-case scenario.

Monthly Premium

The monthly premium is the most visible cost, and it is usually what people focus on first. In my case, the premium came out to $68 per month after subsidies. Without subsidies, the same plan would have cost around $310 per month.

This shows how powerful subsidies can be when searching for cheap health insurance USA. If your income qualifies, you can reduce your monthly costs significantly.

Paying $68 per month means I spend about $816 per year just to stay insured. That is a manageable amount compared to many plans that cost $400 or more per month.

However, a low premium comes with trade-offs. This plan has a higher deductible, which means I need to pay more upfront if I need medical care.

Still, for someone who rarely visits the doctor, this monthly cost is a huge win. It keeps me protected without draining my budget.

Deductible

The deductible for my plan is $7,200 per year. This might sound high, and honestly, it is. But this is the trade-off for having a low monthly premium.

A high deductible means I pay most medical costs out of pocket until I reach that amount. After that, the insurance starts covering a larger share of expenses.

This type of structure works best for people who:

- Are generally healthy

- Do not expect frequent medical visits

- Want to minimize monthly expenses

If you have regular medical needs, this type of plan might not be ideal. You could end up paying more overall despite the low premium.

Still, for many individuals looking for affordable health plans USA, high-deductible plans offer the lowest entry cost into the insurance system.

Out-of-Pocket Costs

The out-of-pocket maximum for my plan is $8,500 per year. This is the absolute most I would pay in a worst-case scenario. Once I reach this limit, the insurance covers 100% of covered services.

This number is important because it defines your financial risk. Even though the deductible is high, the out-of-pocket maximum provides a safety net.

In a normal year, I expect my costs to stay very low. But if something serious happens, I know the maximum financial impact I could face.

When evaluating the lowest health insurance cost USA, always look at this number. It tells you how much protection the plan actually offers.

Cheapest Health Insurance Providers in the USA

Not all insurance companies offer the same pricing or value. Some consistently provide better options for people searching for cheap health insurance USA.

Based on my research, the following providers often offer competitive low-cost plans:

- Blue Cross Blue Shield

- Kaiser Permanente

- UnitedHealthcare

- Aetna

- Cigna

Each provider has strengths and weaknesses. For example, Kaiser Permanente often offers lower premiums but requires you to stay within its network. Blue Cross Blue Shield provides broader coverage but may cost slightly more.

The key is to compare plans within your local area. Prices and availability can vary significantly by state.

Choosing the right provider is just as important as choosing the right plan. A cheap plan from a reliable provider is always better than a slightly cheaper plan with poor service.

Comparison Table of Top Low-Cost Plans

| Provider | Monthly Premium | Deductible | Out-of-Pocket Max | Plan Type |

|---|---|---|---|---|

| Kaiser Permanente | $65 | $7,000 | $8,200 | HMO |

| Blue Cross Blue Shield | $72 | $6,800 | $8,500 | PPO |

| Aetna | $70 | $7,200 | $8,700 | EPO |

| UnitedHealthcare | $75 | $6,500 | $8,300 | PPO |

This table highlights how close these plans are in pricing. Small differences in premium can lead to bigger differences in overall cost depending on usage.

Who Should Choose Cheap Plans

Cheap health insurance plans are not for everyone, but they can be a smart choice for certain groups. Understanding whether you fit into this category can save you a lot of money.

These plans work best for:

- Young and healthy individuals

- Freelancers or self-employed workers

- People with limited budgets

- Those who rarely visit doctors

If you fall into one of these categories, choosing the best budget health insurance USA option can help you stay covered without overspending.

However, if you have chronic conditions or expect frequent medical visits, a low-cost plan might not be the best choice. In such cases, paying a higher premium for better coverage can actually save money in the long run.

Pros and Cons of Low-Cost Insurance

Choosing affordable health plans USA comes with both advantages and disadvantages. It is important to understand both sides before making a decision.

Pros:

- Low monthly premiums

- Financial protection against emergencies

- Access to essential healthcare services

Cons:

- High deductibles

- Limited provider networks

- Higher out-of-pocket costs

Balancing these factors is key to making a smart choice.

Tips to Get Cheaper Health Insurance

If you want to find the lowest health insurance cost USA, these tips can help:

- Always check for subsidies

- Compare multiple plans

- Consider high-deductible options

- Choose in-network providers

- Review plans annually

Small actions can lead to big savings over time.

Common Mistakes to Avoid

Many people make simple mistakes that cost them hundreds or even thousands of dollars each year. Avoiding these can help you get the most value from your plan.

One common mistake is focusing only on the monthly premium. This can lead to choosing a plan with high hidden costs. Another mistake is ignoring provider networks, which can result in unexpected bills.

People also forget to update their plans annually. Insurance markets change, and better options may become available each year.

Avoiding these mistakes is just as important as finding the right plan.

Real Example or Case Study

To make this more real, let’s look at a simple case. A 28-year-old freelancer with no major health issues wanted to reduce expenses. After comparing plans, they chose a high-deductible option with a $70 monthly premium.

Over the year, they only visited a doctor twice and spent about $300 out of pocket. Their total annual cost stayed under $1,200, which is significantly lower than traditional plans.

This example shows how choosing the right cheap health insurance USA plan can lead to real savings.

Conclusion

Finding the cheapest health insurance plan in the US is not impossible. It just requires a bit of effort, smart comparison, and a clear understanding of your needs.

The plan I found costs just $68 per month, but the real value comes from knowing exactly what I am getting and what I might pay in different situations. That clarity is what most people miss.

If you want to save money, start comparing plans today. Look beyond the premium, check your eligibility for subsidies, and choose a plan that fits your lifestyle.

The right plan can protect your health and your wallet at the same time.

FAQs

1. What is the cheapest health insurance in the USA?

The cheapest plans are usually high-deductible marketplace plans with subsidies, sometimes costing under $70 per month.

2. Can I get affordable health plans USA without a job?

Yes, you can use the Health Insurance Marketplace and qualify for subsidies based on your income.

3. Is cheap health insurance worth it?

It depends on your health needs. For healthy individuals, it can be a cost-effective option.

4. How can I lower my health insurance premium?

You can apply for subsidies, choose a high-deductible plan, and compare multiple providers.

5. What is the lowest health insurance cost USA per month?

Some subsidized plans can go as low as $0 to $70 per month depending on eligibility.

Author

Written by: Ahsan Ali

With years of experience analyzing insurance markets and personal finance trends, the author focuses on simplifying complex topics into practical, easy-to-understand advice.